When you apply for a loan, you’re not just submitting paperwork — you’re presenting your entire financial profile for scrutiny. Lenders analyze dozens of variables simultaneously, and a single weak point can derail an otherwise solid application. Understanding what triggers approvals, denials, and follow-up requests gives you a strategic advantage most applicants never have. What lenders actually examine goes far deeper than your credit score alone.

Table of Contents

In a Nutshell

- Lenders evaluate credit scores and payment history to assess a borrower’s reliability in honoring financial obligations.

- Debt-to-income ratio must typically stay below 43% for conventional lenders to approve loan applications.

- Income verification through tax returns and pay stubs confirms a borrower’s ability to repay loans.

- Collateral and loan-to-value ratios help lenders measure risk, often resulting in lower interest rates for secured loans.

- Red flags like excessive inquiries, income inconsistencies, and derogatory marks can trigger automatic application denials.

What Type of Loan You’re Applying for Changes Everything

The type of loan you’re applying for shapes every aspect of how a lender evaluates your application. Different loan types carry distinct risk profiles, collateral requirements, and qualification thresholds.

A mortgage demands income verification, credit history, and property appraisal. A personal loan weighs your debt-to-income ratio more heavily. A business loan scrutinizes cash flow projections and operational history.

Each loan type triggers a specific application process with tailored documentation requirements. Understanding these distinctions before you apply lets you anticipate lender expectations, prepare accurate materials, and position yourself as a qualified borrower from the start. For example, secured loans typically offer lower interest rates than unsecured loans because the lender’s risk is reduced by the collateral backing the debt.

Your Credit Score and What It Signals to Lenders

Creditworthiness, distilled into a three-digit number, tells lenders more about your financial behavior than almost any other single metric.

Your credit score synthesizes complex borrowing patterns into an instantly readable risk signal. Lenders parse it quickly, and it directly influences approval odds, interest rates, and loan terms.

Key factors your score communicates:

- Payment history reveals if you honor financial obligations consistently

- Credit utilization indicates how much available credit you’re actively carrying

- Derogatory marks signal past defaults or delinquencies

- Account age demonstrates long-term credit management

- Hard inquiries suggest recent, potentially aggressive borrowing behavior

Your Credit History Beyond Just the Score

While your credit score offers lenders a quick snapshot, your full credit report delivers the granular detail that shapes their final decision.

They’ll scrutinize your payment history, identifying patterns of late or missed payments. They’ll assess your credit utilization, flagging ratios exceeding 30%.

Recent inquiries signal financial stress if clustered tightly. Your account types and credit mix demonstrate your capacity to manage diverse debt instruments.

Derogatory marks—collections, charge-offs, bankruptcies—carry significant weight. Understanding these components accelerates meaningful credit improvement by targeting specific weaknesses.

Your financial behavior over time communicates trustworthiness far more powerfully than any single three-digit number ever could. If you’re uncertain where you stand, free tools like ExtraCredit provide FICO scores from all three bureaus, giving you a comprehensive view of your credit profile before applying.

Why Credit Age Matters to Lenders

Among the factors lenders analyze, credit age carries more weight than many borrowers realize. It signals financial stability and responsible long-term credit management.

Credit age quietly shapes your financial reputation, revealing a history of stability that lenders trust above nearly everything else.

Lenders evaluate your oldest account, newest account, and average account age collectively. High credit utilization or excessive credit inquiries can further damage a young credit profile.

Key elements lenders assess regarding credit age:

- Average age of all open accounts

- Age of your oldest active account

- How recently you’ve opened new accounts

- Impact of credit inquiries on account history length

- Relationship between credit utilization rates and account maturity

How Lenders Verify Your Income and Employment

Beyond credit history, lenders scrutinize your income and employment to confirm you can actually repay what you’re borrowing.

They’ll request income documentation—typically two years of tax returns, recent pay stubs, and W-2s—to calculate your stable monthly earnings.

Employment verification follows, where lenders contact your employer directly or use third-party services to confirm your job title, tenure, and status.

Self-employed borrowers face stricter scrutiny, often requiring profit-and-loss statements and business bank records.

Lenders compare your verified income against existing debt obligations, establishing your debt-to-income ratio, which directly determines your borrowing eligibility and loan terms.

Why Your Debt-to-Income Ratio Can Make or Break Approval

Your debt-to-income ratio (DTI) is one of the most decisive factors in a lender’s approval decision, calculated by dividing your total monthly debt obligations by your gross monthly income.

Strong debt management directly shapes this metric, signaling your financial stability to underwriters.

Disciplined debt management defines your DTI, proving financial reliability to the lenders who determine your borrowing future.

- Most conventional lenders prefer a DTI below 43%

- Front-end DTI covers housing costs only

- Back-end DTI includes all recurring debt obligations

- Lower DTI demonstrates disciplined financial stability

- High DTI signals overleveraging and repayment risk

Reducing existing balances before applying strategically improves your ratio and strengthens your overall application profile. Strategies such as refinancing for lower interest rates on outstanding loans can meaningfully reduce your monthly debt obligations, bringing your DTI into a more favorable range before a lender reviews your application.

Your Loan-to-Value Ratio and Why Lenders Care

While your DTI tells lenders how much of your income is already spoken for, the loan-to-value ratio (LTV) tells them how much skin you have in the game.

LTV measures your loan amount against the asset’s appraised value. A lower LTV signals stronger loan equity, reducing the lender’s exposure if you default. Most lenders prefer an LTV at or below 80%. Above that threshold, you’ll typically face higher rates or mandatory mortgage insurance.

LTV is central to risk assessment because it quantifies collateral coverage. The more you bring to the table upfront, the safer the loan looks to underwriters.

The Role of Collateral in Secured Loan Approvals

Collateral gives lenders a tangible fallback when a borrower defaults, converting an unsecured promise to repay into a claim against a specific asset.

Collateral valuation determines how much risk the lender actually absorbs, while collateral types influence approval odds and loan terms considerably.

Key factors lenders assess:

- Asset liquidity — how quickly they can convert collateral to cash

- Current market value versus outstanding loan balance

- Depreciation rate of the pledged asset over the loan term

- Title clarity — whether liens or encumbrances cloud ownership

- Collateral type alignment with the loan’s purpose and structure

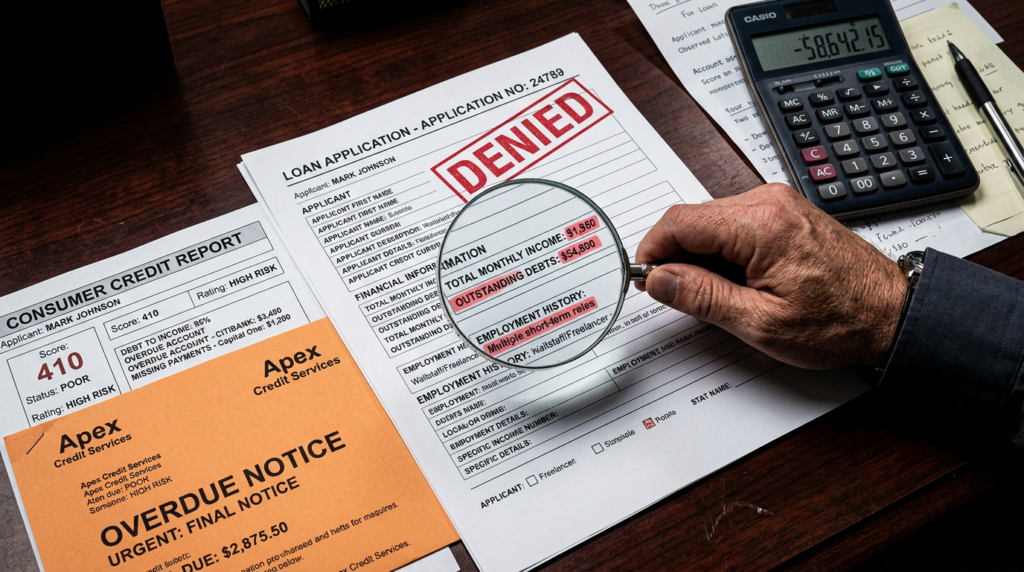

Red Flags That Trigger Automatic Loan Denials

Even strong collateral won’t save a loan application riddled with disqualifying signals that lenders flag before they ever weigh asset value.

Application inconsistencies between stated income and income verification documents immediately raise borrower red flags. Excessive credit inquiries suggest financial instability and desperation. Unexplained rapid changes in employment, assets, or addresses undermine demonstrated financial stability.

Unresolved previous defaults communicate systemic repayment failure. Vague or suspicious loan purpose descriptions conflict with lender preferences for transparent fund usage. Disproportionate debt obligations relative to income trigger automatic disqualification thresholds.

Lenders apply algorithmic and manual screening simultaneously, eliminating compromised applications before human underwriters invest deeper analytical resources.

How to Strengthen a Weak Loan Application

Strengthening a weak loan application requires targeting the specific deficiencies lenders flag during initial screening rather than broadly improving peripheral factors.

Use alternative documentation—bank statements, tax transcripts, or asset verification letters—to compensate for income inconsistencies. Borrower education programs can demonstrate financial responsibility, sometimes offsetting marginal credit scores.

- Reduce your debt-to-income ratio before reapplying

- Add a creditworthy co-borrower to offset risk

- Increase your down payment to lower LTV ratios

- Dispute inaccurate derogatory marks on credit reports

- Provide written explanations for previous delinquencies

Address each weakness systematically; lenders respond to documented, measurable improvements rather than vague corrective promises. If you cannot qualify independently, a cosigner with strong credit can significantly improve approval odds, though late payments will affect both parties’ credit scores.

What to Do If You’re Denied a Loan

When a lender denies your application, the first step is obtaining the adverse action notice, which federal law requires lenders to issue within 30 days. This document outlines the specific reasons for denial, giving you a clear diagnostic starting point.

Review it carefully—whether it’s insufficient income, poor credit history, or high debt-to-income ratio, each reason maps directly to correctable financial behaviors.

Every denial reason—low income, poor credit, high debt—points directly to a financial behavior you can fix.

Your next steps should include disputing inaccurate credit report entries, addressing deficiencies, and reapplying once you’ve made measurable improvements.

You can also consider alternative lenders, credit unions, or secured loan products that accommodate your current financial profile.

Frequent Questions and Answers

Can Applying for Multiple Loans Simultaneously Hurt Your Approval Chances?

Yes, applying for multiple loans simultaneously can hurt your approval chances. Each application triggers hard credit inquiries, and their impact timing matters—lenders see clustered inquiries as financial desperation, greatly reducing your creditworthiness and approval probability.

Do Lenders Consider Your Savings or Investment Accounts During Review?

If you’ve got $50K in index funds, lenders notice. Your savings impact their risk assessment, and your investment stability signals you can weather financial setbacks—making you’re a far more creditworthy borrower overall.

How Long Does the Loan Approval Process Typically Take?

You’ll typically wait 2–7 business days to several weeks, depending on loan processing timelines and factors affecting duration, such as loan type, document completeness, lender workload, and your credit complexity—all directly influencing how quickly you’ll receive approval.

Can a Co-Signer Improve Your Chances of Getting Approved?

Yes, a co-signer can greatly boost your approval odds. You’ll utilize their strong credit history, and lenders recognize the shared financial responsibility, amplifying co-signer benefits that offset your perceived risk and strengthen your overall application considerably.

Are Loan Approval Criteria Different for Self-Employed Versus Salaried Applicants?

Ah, because lenders *love* uncertainty! If you’re self-employed, you’ll face stricter scrutiny—lenders require extensive tax documentation to verify your self-employment income, unlike salaried applicants who simply present pay stubs. Yes, the criteria differ considerably.

Conclusion

Getting approved for a loan isn’t luck—it’s strategy. Think of your application like a job interview: every detail you present either builds or breaks the lender’s confidence in you. Studies show borrowers who address weaknesses proactively are 40% more likely to secure approval. You now understand what lenders scrutinize, from credit behavior to collateral strength. Use that knowledge deliberately, and you’ll walk into any lending conversation from a position of informed control.